COVID-19 has challenged almost all businesses

Signs of a two-speed recovery are emerging: few sectors are benefitting from increased demand, while many more face slow growth, and sectors such as tourism and automotive grapple with challenges. Online sales are a feature of outperformance.

The pandemic has dampened business optimism. A majority (53%) have poorer growth expectations than in the 2019 survey and profits are above pre-pandemic levels in only 8% of firms. Expectations of future revenue growth have dropped by 15 percentage points since 2019, with two-thirds of businesses (64%) projecting revenue growth next year. And a quarter of companies globally (24%) expect declining revenues over the next year. A resurgence in COVID-19 cases is the primary threat to growth and recovery.

53%

of businesses have poorer growth expectations than in the 2019 survey

Key HSBC GDP forecasts*

| 2020f | 2021f | 2022f | |

| World | -4.1% | 4.7% | 3.1% |

| Developed | -5.6% | 4.0% | 2.3% |

| Emerging | -2.0% | 5.6% | 4.1% |

| US | -4.1% | 3.1% | 2.5% |

| Mainland China | 2.4% | 7.5% | 5.6% |

| Eurozone | -7.6% | 5.7% | 2.5% |

* HSBC Economics, Bloomberg

The profile of profitability reveals a lengthy recovery for many sectors. Half of firms globally expect to return to pre-COVID levels of profits this year or 2021 (53%). On the other hand, for nine in 20 firms, pre-pandemic profitability is not expected to return until 2022 or later. This is consistent with HSBC economic forecasts which do not project a sharp ‘V-shaped’ recovery, at least in terms of levels of activity.

A narrower set of leading companies is emerging, with 15% of firms projecting growth of over 15% this year (a third lower than in 2019). As the pandemic reduced social contact, having an online presence enhanced business performance. Online businesses are more optimistic about future prospects, and this trend extends across the technology, IT and telecommunication sectors. Businesses in sectors such as advertising and PR, food and pharmaceuticals also reported an increase in demand thanks to the COVID-19 pandemic.

At the other end of the spectrum, the proportion of no-growth companies has doubled in a year. And while a majority of firms expect to grow between 2 and 15%, this grouping has reduced by seven percentage points since 2019, reflecting growing pessimism.

A quarter (24%) identify as thriving, against a fifth (19%) that identify as surviving. Fewer than one in five businesses in tourism (15%) and automotive (17%) expect to return to pre- pandemic profitability this year. Components manufacturers are particularly vulnerable, relying on upstream demand.

Within Asia, open economies such as Hong Kong, Singapore and South Korea reportedly face greater challenges, whereas strong optimism permeates emerging markets such as Bangladesh, Vietnam and India. Businesses in the Americas and the Middle East are most optimistic with European firms most pessimistic about growth.

Most and least challenged sectors

Current status of business

| Thriving in the new normal % | Surviving day to day % | |

| Oil and gas | 40 | 13 |

| Infrastructure | 37 | 18 |

| Metals / Mining | 34 | 17 |

| Power / Utilities | 30 | 21 |

| Pharma | 30 | 10 |

| 15 other sectors | 24-26 | |

| Advertising | 14 | 26 |

| Arts | 13 | 28 |

| Media / Films | 13 | 31 |

| Tourism | 11 | 26 |

| Manufacturing – Glass | 10 | 29 |

We have been working with a certain mix of service offerings for a long time. This was one of those journeys where we challenged that. We had a certain way of doing business for many years. This was the first year we challenged it…

Expected sales growth over the next year

| 2019 | 2020 | |

| 15%+ growth | 22% | 15% |

| 2-15% growth | 57% | 50% |

| Sales flat | 8% | 11% |

| Sales declining | 12% | 24% |

I think the hardest thing is that I probably had to focus on the latest Quarter more than I felt I should, when I really wanted to look after 2020, 2021 and 2022.

How business outlook has changed over the past 12 months*

| More pessimistic | More optimistic or expect to stay the same | |

| Asia Pacific 2019 Asia Pacific 2020 |

20% 32% |

80% 68% |

| Europe 2019 Europe 2020 |

20% 36% |

79% 62% |

| North America 2019 North America 2020 |

12% 26% |

88% 73% |

| South America 2019 South America 2020 |

13% 18% |

86% 80% |

| Middle East & North Africa 2019 Middle East & North Africa 2020 |

15% 22% |

85% 77% |

| Rest of Africa 2019 Rest of Africa 2020 |

18% 32% |

82% 67% |

*Excludes businesses answering "Don't know'

Asia: divergent outlooks

Expectations of sales growth in the next year have declined in Asia Pacific, going from just under four out of five (77%) in 2019 to three out of five (60%) businesses in 2020 expecting sales growth.

However, there is wide variability of sales expectations within the region – featuring the most positive (Indonesia) growth – as well as the most negative (Japan) markets across all 39 markets surveyed.

Proportion of businesses that expect growth of overall sales in the next year

| Indonesia | Mainland China | South Korea | Japan | |

| 2019 | 99% | 86% | 64% | 57% |

| 2020 | 91% | 62% | 46% | 35% |

E-commerce has driven growth

Proportion of business sales coming from online

The movement to online has been dramatic… every retailer, every market with online commerce has gone up.

Winning strategies

The 2003 SARS epidemic catalysed mainland China’s development as the world’s leading e-commerce market, now larger than the next ten markets combined.1

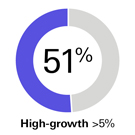

This pandemic is accelerating that trend globally, as digitally enabled businesses serve customers online. High-growth firms now make a majority of sales online.2

The proportion of consumers that are digital natives will double this decade, creating compelling opportunities.3

1 McKinsey: China digital consumer trends 2019

2 51% high-growth firms (annual revenue growth >5%) are >50% online.

3 HSBC Global Research, The booming digital economy, September 2020