- Article

- Global Investment Research

- Understand ESG

- General Research Insights

Sustainability in 2026: Net zero navigator

The race to a global net-zero emission operating system is increasingly determined by economic competitiveness over politics. This creates opportunities in the countries that have already created an enabling environment driving down the cost of cleaner energy and have an economic diversification strategy, such as China and the Middle East. Pragmatism rules, however, as countries acknowledge that adapting to warmer temperatures is part of maintaining productivity.

2026 in one word – pragmatism

We expect the sustainability agenda in 2026 to be characterised by a pragmatism towards a country’s ability to implement climate plans based on economics alone, and a greater acceptance that finance requirements have to come from somewhere other than public coffers.

Being pragmatic about a country’s ability to deliver climate outcomes does not mean that the goal of controlling emissions to limit temperature rises is off the table. It means recognising that letting perfection get in the way of progress has not achieved peak emissions or speed of decline in time to limit temperature rises to below 1.5°C. 2026 will be a reality check on how and where climate plan delivery is moving forward at pace and identifying transition funding.

Pragmatism is not defeatist or sitting on the fence but adaptation is a higher priority in 2026.

A pragmatic approach is also not the same as country or corporate indifference on how an energy transition can be achieved. It means prioritising an approach that makes sense for the country resource availability and competitiveness, and adopting a strategy to deliver based on those foundations. Countries are doing this through nationally determined contributions, and companies are working on transition plans.

The lack of speed on delivering emissions control means that we expect adaptation topics to be back in focus for investors in 2026. Temperature rises are hovering around the 1.4-1.5°C mark, according to the European Commission Copernicus service, so unpredictable weather-related disruption is likely to continue to occur.

While investors can sense-check if companies have robust, diverse supply chains and operating facilities to be resilient on a location basis, inevitably large location-based operational disruption surprises would likely to create valuation swings to corporates exposed in those regions, and create disruption to economic activity.

Adaptation efforts are wide-reaching and can include cooling facilities for people to remain productive when countries are heat stressed, urban heat reduction, water-management systems to manage flooding, and R&D spend on the warming effects on health and food systems. Adaptation finance has been hard to access previously because of the complexity on modelling investment benefits, but work is ongoing in this area and we expect progress through 2026, driven by a renewed country focus on adaptation plans.

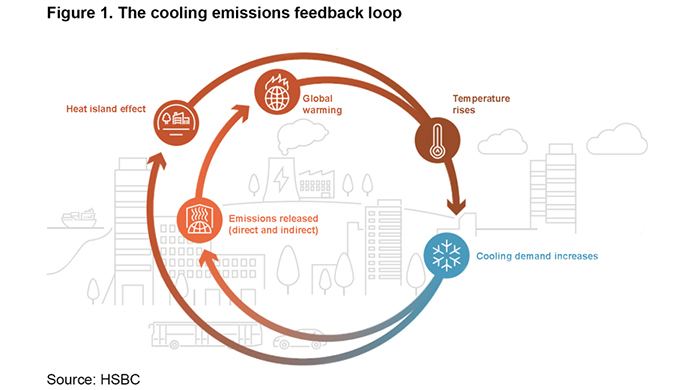

These adaptation plans are increasing, including sustainable cooling strategies to adapt to the rising climate risks. Cooling itself faces a climate conundrum, with emissions risks that exacerbate climate change impacts. However, as initiatives such as the Global Cooling Pledge and the alignment of NAPs and NDCs progress, sustainable cooling solutions ease emission risks while providing adaptation benefits.

Transparency on transition finance plays to a pragmatic approach for capital provision.

While transparency on funding for pure-play green activities is well marked out through the green bond market, a transition finance label has been harder for a consensus to agree on. ICMA1, the architect of the Green Bond Principles, published transition guidelines and a handbook in November. This should help investors categorise positive outcomes from a transition strategy in high-emission and hard-to-abate sectors.

Most climate indicators are backward looking, since they reflect facts and are often released months later. The most coincident climate metric example is CO2 concentration data recorded daily at Mauna Loa in Hawaii, currently at 428ppm2. While these data points have been useful in the past to raise awareness about the status of climate activity, we expect investors to become more demanding about linking data points to a forward-looking signal on the speed of transition. From a macro perspective, trade flows warrant a closer look, since a country’s competitive advantage in low-carbon activity will be a growth driver. At a micro level, capex flows signal how fast low-carbon activity will play out.

In conclusion, a pragmatic approach means that we expect investors to adopt new ways of anticipating the speed of transition in 2026.

Would you like to find out more? Clients of HSBC Global Investment Research can click here* to read the full report.

To learn more about HSBC Global Investment Research, including how to subscribe, please email us at AskResearch@hsbc.com

*Please note that by clicking on this link you are leaving the HSBC Corporate & Institutional Banking website, therefore please be aware that the external site policies will differ from our website terms and conditions and privacy policy. The next site will open in a new browser window or tab

- International Capital Markets Association, Climate Transition Bond Guidelines, November 2025

- Reading at 15 January 2026

The following analyst(s), who is(are) primarily responsible for this document, certifies(y) that the opinion(s), views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Zoe Knight

This document has been issued by the Research Department of HSBC.

HSBC and its affiliates will from time to time sell to and buy from customers the securities/instruments, both equity and debt (including derivatives) of companies covered in HSBC Research on a principal or agency basis or act as a market maker or liquidity provider in the securities/instruments mentioned in this report.

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment banking, sales & trading, and principal trading revenues.

Whether, or in what time frame, an update of this analysis will be published is not determined in advance.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that company available at www.hsbcnet.com/research.

Additional disclosures

- This report is dated as at 19 January 2026.

- All market data included in this report are dated as at close 15 January 2026, unless a different date and/or a specific time of day is indicated in the report.

- HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

- You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of a financial instrument or of an investment fund.

- Zoe Knight is a Non-Executive Director of HSBC UK Bank Plc.

This document has been issued by HSBC Bank Middle East Ltd, DIFC, which has based this document on information obtained from sources it believes to be reliable but which it has not independently verified. Neither HSBC Bank Middle East Ltd, DIFC nor any member of its group companies (“HSBC”) make any guarantee, representation or warranty nor accept any responsibility or liability as to the accuracy or completeness of this document and is not responsible for errors of transmission of factual or analytical data, nor is HSBC liable for damages arising out of any person’s reliance on this information. The information and opinions contained within the report are based upon publicly available information at the time of publication, represent the present judgment of HSBC and are subject to change without notice.

This document is not and should not be construed as an offer to sell or solicitation of an offer to purchase or subscribe for any investment or other investment products mentioned in it and/or to participate in any trading strategy. It does not constitute a prospectus or other offering document. Information in this document is general and should not be construed as personal advice, given it has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Accordingly, investors should, before acting on it, consider the appropriateness of the information, having regard to their objectives, financial situation and needs. If necessary, seek professional investment and tax advice.

The decision and responsibility on whether or not to purchase, subscribe or sell (as applicable) must be taken by the investor. In no event will any member of the HSBC group be liable to the recipient for any direct or indirect or any other damages of any kind arising from or in connection with reliance on any information and materials herein.

Past performance is not necessarily a guide to future performance. The value of any investment or income may go down as well as up and you may not get back the full amount invested. Where an investment is denominated in a currency other than the local currency of the recipient of the research report, changes in the exchange rates may have an adverse effect on the value, price or income of that investment. In case of investments for which there is no recognised market it may be difficult for investors to sell their investments or to obtain reliable information about its value or the extent of the risk to which it is exposed. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors.

This document is for information purposes only and may not be redistributed or passed on, directly or indirectly, to any other person, in whole or in part, for any purpose. The distribution of this document in other jurisdictions may be restricted by law, and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. By accepting this report, you agree to be bound by the foregoing instructions. If this report is received by a customer of an affiliate of HSBC, its provision to the recipient is subject to the terms of business in place between the recipient and such affiliate. The document is intended to be distributed in its entirety. Unless governing law permits otherwise, you must contact a HSBC Group member in your home jurisdiction if you wish to use HSBC Group services in effecting a transaction in any investment mentioned in this document.

Certain investment products mentioned in this document may not be eligible for sale in some states or countries, and they may not be suitable for all types of investors. Investors should consult with their HSBC representative regarding the suitability of the investment products mentioned in this document.

HSBC and/or its officers, directors and employees may have positions in any securities in companies mentioned in this document. HSBC may act as market maker or may have assumed an underwriting commitment in the securities of companies discussed in this document (or in related investments), may sell or buy securities and may also perform or seek to perform investment banking or underwriting services for or relating to those companies and may also be represented on the supervisory board or any other committee of those companies.

From time to time research analysts conduct site visits of covered issuers. HSBC policies prohibit research analysts from accepting payment or reimbursement for travel expenses from the issuer for such visits.

HSBC Bank Middle East Ltd (“HBME”) is incorporated in the Dubai International Financial Centre, regulated by the Central Bank of the U.A.E and the Securities and Commodities Authority-License No. 602004, and lead regulated by the Dubai Financial Services Authority. Within UAE, HBME issues Research via HSBC Bank Middle East Limited, DIFC, located within the Dubai International Financial Centre and regulated by the Dubai Financial Services Authority, as well as through HSBC Bank Middle East Limited UAE branch, regulated by the Securities and Commodities Authority under License No. 602004 (Fifth Category) for Financial Consultation and Financial Analysis.

© Copyright 2026, HSBC Bank Middle East Ltd, DIFC ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the issuer of the report.

Issuer of report

HSBC Bank Middle East Ltd, DIFC

HSBC Sustainability Sentiment Survey

What are investors thinking about sustainability now?